In February 2026, the BSP circulated a draft rule that rattled the rural banking sector: cap the share of accounts a rural bank can hold outside its home turf at 30 percent, or get reclassified as a digital bank, with the jump to a Php 1 billion minimum capital requirement that comes with it. Industry groups pushed back hard. The concern is real: rural banks want to modernize without accidentally becoming something the regulator (and their balance sheet) can't support.

But the digitalization that actually moves a rural bank's loan book has very little to do with how far its mobile app reaches. It's what happens between the teller's desk and the credit committee: how a loan file gets read, checked, and decided. That's back office, not "digital reach," and it's where most of the real cost and risk in rural lending actually sits.

The paperwork problem doesn't look like a tier-1 bank's

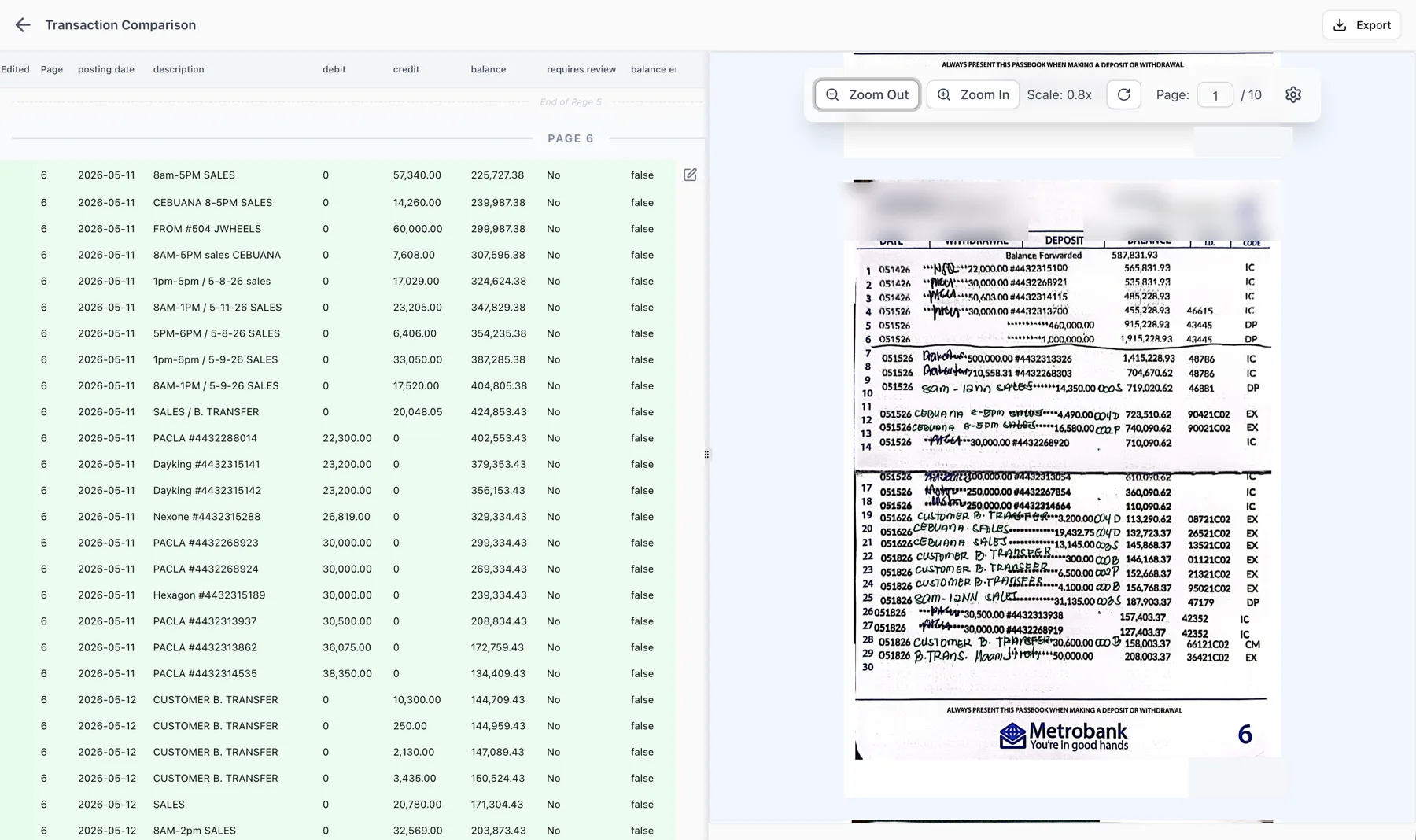

A rural bank's loan file rarely looks like the clean PDF bank statement an IDP vendor demoed to its investors. It looks like a passbook with a teller's handwriting across three different pens. A barangay certificate photographed at an angle on someone's phone. A farmer's income built from a season's worth of receipts and a co-op ledger, not a payslip.

Generic OCR and the IDP tools built for pristine, digital-native documents choke on exactly this kind of paperwork, or they hand it back to a loan officer to rekey by hand. That rekeying step is where a rural bank's real cost lives: not in software, but in headcount spent typing numbers off a passbook into a spreadsheet, one application at a time.

We built Floowed's document intelligence for this end of the spectrum: handwritten, scanned, and photographed loan documents, read natively, not bounced back for manual entry. It's the same extraction engine whether the input is a passbook, a barangay certificate, or a bank statement, and it's genuinely ahead of the US-built IDPs that optimized for pristine documents a rural bank borrower rarely produces.

The scale problem RBAP keeps raising is a document intelligence problem

The Asian Development Bank recently granted around ₱36.7 million to eight rural banks for cloud-based core banking, loan origination, and credit scoring systems. That's a meaningful start, and it says something important: the industry already knows it needs this. But grant funding for eight banks doesn't reach the hundreds of rural banks that never get picked for a pilot, and most of them will have to fund modernization themselves.

That's a real constraint. The typical rural bank doesn't have the size to absorb the cost of building or buying a capable digital solution on its own, and that's a fair description of what tier-1 loan origination and decisioning platforms actually cost, in money and in implementation time.

| Capability | Generic OCR / IDP | Tier-1 decisioning platform | Floowed |

|---|---|---|---|

| Handwritten passbooks, photographed IDs | Fails or needs rekeying | Assumes clean digital input | Reads them natively |

| Implementation | Integration project on top | 6 to 18 months, consulting-led | Weeks of configuration, then live |

| Policy on the extracted data | Separate tool, manual | Bundled, but PS-dependent to change | Same platform, credit and risk teams maintain it directly |

A rural bank doesn't need tier-1 scale to get tier-1 rigor. It needs a platform sized so the implementation doesn't cost more than the problem it's solving, without giving up the document-reading capability that a rural loan book actually requires.

Modernizing the back office doesn't touch BSP's digital-reach concern

It's worth separating two things the draft circular tends to blur together in the sector's conversation. One is digital reach: onboarding customers outside a bank's home territory, branchless account opening, the kind of geographic expansion the BSP is trying to keep proportional to a rural bank's capital base. The other is underwriting infrastructure: how a loan application that already walked into a branch gets read, scored, and decided.

Document intelligence and a decisioning engine sit entirely in the second category. Reading a passbook faster and enforcing a consistent credit policy on it doesn't expand a rural bank's footprint or its customer base outside its charter. It makes the lending the bank is already licensed to do faster and more consistent, which is a different kind of digitalization than the one the draft circular is worried about.

From a stack of documents to a decision an examiner can follow

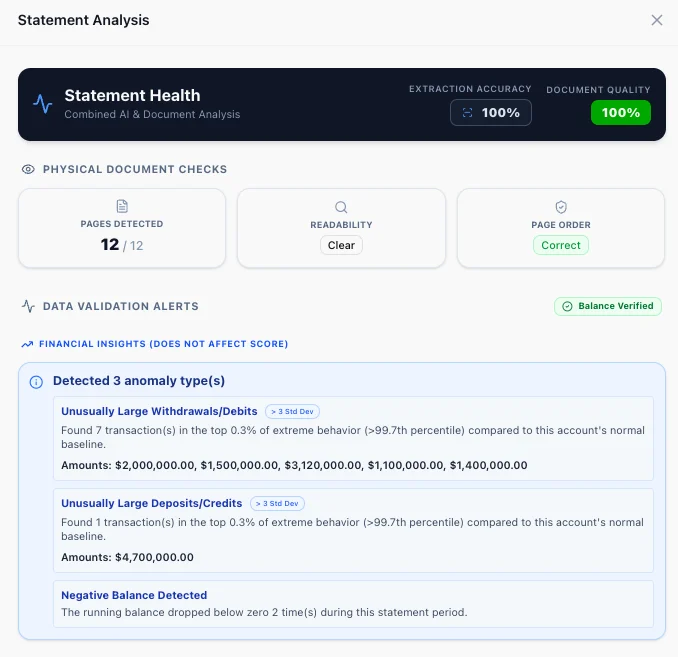

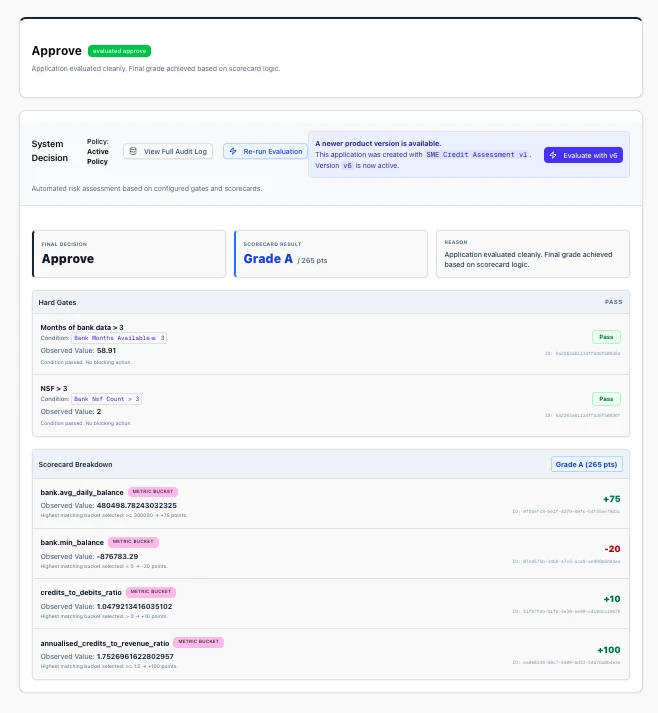

The harder part isn't reading the documents. It's making sure the same credit policy actually applies the same way to every application, across every branch and every loan officer, and that there's a record of it when an examiner or an internal auditor asks why a specific loan was approved or declined.

That's the second half of what we do: a Decisioning Engine that runs the policy your credit and risk team writes, identically, on every application, with full version history and an audit trail attached. Change a cutoff, add a rule for co-op-guaranteed loans, adjust for a seasonal agricultural cycle: the policy you write is the policy that runs, not a suggestion a branch can quietly override.

We're also score-agnostic. A rural bank that already pulls CIC or CMAP reports, or runs its own internal scorecard, keeps doing that. We process what the bank brings in: no need to switch bureau accreditation or replace a scoring model the bank already trusts.

What this looks like for a credit and risk team, in weeks, not quarters

None of this requires a rural bank to run a multi-quarter implementation with an outside consulting team, and none of it requires an engineering team the bank doesn't have. Configuration takes weeks, not the quarters a tier-1 platform's professional-services process usually takes, and the credit and risk team is the one operating the policy day to day, not waiting on a vendor ticket to change a threshold.

RBAP has spent its 70th year pushing the line that no rural bank should be left behind in digitalization. The version of that worth chasing first isn't a bigger app footprint the regulator has to watch closely. It's a back office that reads what its borrowers actually bring in, and a credit policy that runs the same way every time it's applied.