DECISION ENGINE

The policy you write is the policy that runs.

Your credit and risk teams build the policy: scorecards for the score, hard gates for the must-haves. Back-test it against your real loan performance, then it runs identically on every application, automatically, with a full audit trail behind every decision.

ANATOMY OF A DECISION

Seven layers. One executable policy.

A decision isn't a black box. It's seven layers you build and own, from raw document data to a live application, each one inspectable.

- Data elementsEvery field machine-read from the file: bank analysis, financials, fraud signals, entity research, plus any custom extractor. If it's in the document, you can use it in a decision.

- Synthetic metricsLender-built ratios derived from two or more fields: balance volatility, bank credits vs declared revenue, credits-to-debits, forecast vs actual.

- RulesEach rule is one condition (a threshold, a date age, exists or missing, a fuzzy match) with one action: auto-reject or send to manual review. Combine rules in a policy for AND/OR logic.

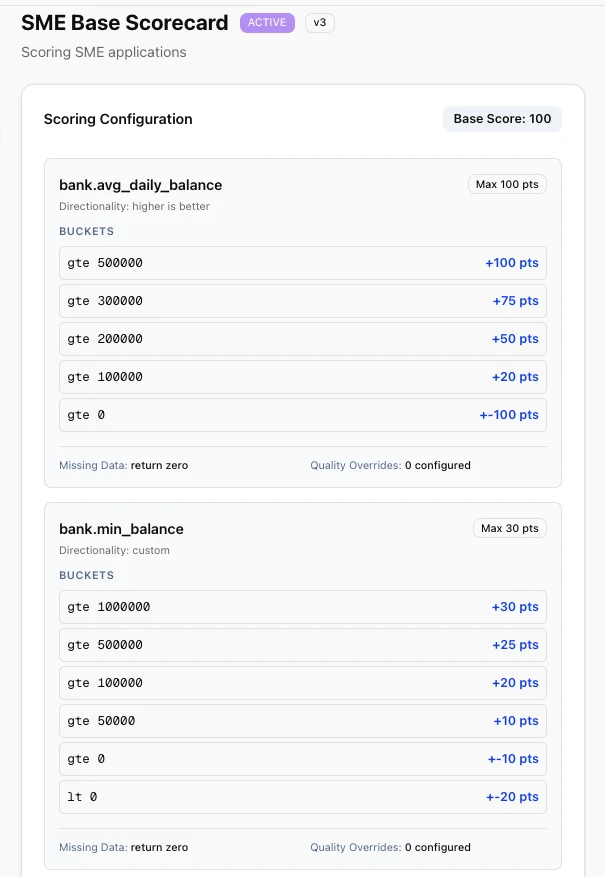

- ScorecardsWeighted, banded points by value range or rule outcome, totalled into a grade. Grade thresholds map to approve, manual review, or reject. Bring any score as an input; you set the weights.

- PoliciesYOUR ASSETTwo separate things: the scorecard for the judgment in between, and hard gates for the must-haves. A hard gate that fails blocks approval no matter how high the score.

- Application templatesBinds a policy to a workflow and its required documents. Pick the template when an application is created and decisioning runs; skip it and it doesn't.

- Live applicationsEvery real application runs the full flow and lands on one outcome you defined: recommended to approve, manual review, or reject. Floowed returns the decision; it never moves money.

SCORECARDS & HARD GATES

Your scoring model, your non-negotiables.

Floowed is score-agnostic: bring the model you already trust and the engine orchestrates policy around it. Hard gates handle the lines that never move, scorecards handle the judgment in between. Floowed weights nothing of its own: you set every weight.

- Bureau, FICO-style, or custom scorecards, absorbed unchanged

- Hard gates for the rules that never bend

- Weighted criteria your credit and risk teams author directly

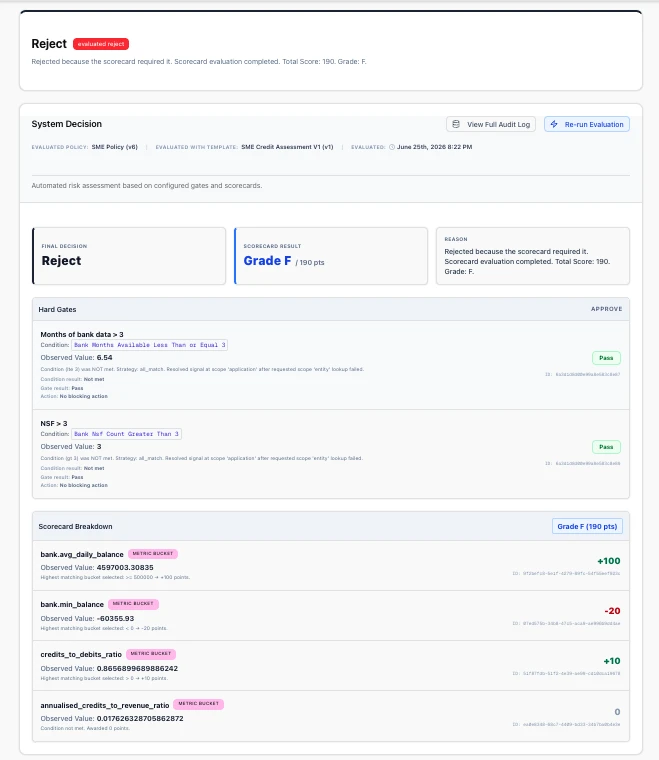

THE DECISION REPORT

Every decision, fully explained.

Open any application and see the whole story: every gate evaluated, every score computed, reason codes on every decline. The full reasoning stays on record, ready for an auditor, a regulator, or your own credit committee.

Walk through a real decisionCHANGE IT SAFELY

Test the change before it touches a real application.

Back-test a new policy against last year's approved and rejected book, scored against how those loans actually performed. Quantify the impact on your approval rate and your NPL before anything ships, measured against real outcomes rather than estimated.

01

Propose

Build the change in the policy builder: a new cutoff, a tightened gate, a re-weighted scorecard. The live policy keeps running untouched.

02

Back-test

Replay the draft against your historical book and how those loans actually performed. Approval-rate and NPL impact, plus every decision that would flip, quantified before you commit.

03

Go live

The change is saved as a new version, the prior version stays intact so past decisions still stand, and the new policy runs on the very next application.

GOVERNANCE

Built to stand up to an audit.

VERSION CONTROL

Every policy change is versioned and attributed: who, what, and when. Prior versions stay intact, so past decisions still stand and you can roll back any time.

BACK-TESTED BEFORE LIVE

Replay any policy change against your historical book and its real outcomes before it runs, so the approval-rate and NPL impact are known, not guessed.

DECISION RECORDS

Every decision keeps the exact documents, data, and policy version that drove it, re-inspectable years later, with reason codes on every outcome.

ROLE-BASED ACCESS

Who can author, approve, and override is set by role, so the right people hold the policy.

SAME POLICY · EVERY APPLICATION · EVERY TIME · NO EXCEPTIONS

QUESTIONS

Loan decisioning, answered.

What is a loan decisioning engine?

A loan decisioning engine is software that executes a lender's credit policy automatically and identically on every application. With Floowed, the policy you write is the policy that runs: the same hard gates, scorecards, and logic applied every time, with no exceptions and a full version history.

How does Floowed keep lending decisions consistent?

Floowed runs one executable policy on every application, so the outcome no longer depends on who reviewed the file. The same rules and scorecards are applied identically each time, on data machine-read from the documents, with an audit trail behind every decision.

Does Floowed replace our scoring model or credit bureau?

No. Floowed is score-agnostic: it absorbs your scoring model unchanged (bureau, FICO-style, or your own) and orchestrates the decision around it. Bring any score; Floowed weights nothing of its own and runs it rather than competing with it.

What can a Floowed credit policy include?

A policy is built in layers: data elements machine-read from the documents, synthetic metrics derived from them (balance volatility, bank credits vs declared revenue, ratios), rules of one condition each, weighted scorecards, and hard gates for the must-haves. A hard gate that fails blocks approval no matter how high the score.

Can credit and risk teams change the policy themselves?

Yes. Weighted criteria, hard gates, and scorecards are authored by your credit and risk teams directly. But the point isn't who edits it; it's that whatever policy you set is then enforced identically on every application, automatically.

Is there an audit trail for every decision?

Yes. Every decision carries a full record of the policy version, the inputs it used, and the rules that fired: a trail your risk team and auditors can follow.

How is a decisioning engine different from a loan origination system (LOS)?

An LOS manages the loan workflow; the decisioning engine makes the credit decision. Floowed sits in front of your LOS: it reads the documents, applies your policy, and returns a recommended decision, then feeds the result downstream across 40+ integrations. Floowed stops at the decision; it does not disburse or service the loan.

ONE PLATFORM

One platform. The whole decision.

The policy is the closer. Here’s what feeds it.

Put your policy in production.

Author it once. Watch it run on a real application.