OR/CR collateral loans (sangla OR/CR)

Lend against the title while the borrower keeps and uses the vehicle. The ORCR read, matched to the unit, and checked for a clean lien, with refinancing on the same rails.

VEHICLE FINANCING

In vehicle lending the collateral is a document. Floowed reads the ORCR or title, photographed, faded, any quality, cross-checks the VIN, make, and owner against the vehicle photos and the rest of the file, checks for an existing lien, then runs your LTV and vehicle-age policy on every application, identically, every time.

WHY THE COLLATERAL IS THE RISK

Vehicle lending looks simple until the paperwork arrives. The unit's identity, its value, and its owner all live in documents that have to agree with each other and with a real car, and most lenders check that by eye, one file at a time, differently from one branch to the next. That is where cloned units slip through, swapped plates get financed, and the borrower on the title turns out not to be the borrower on the IDs.

The collateral is a document, the ORCR or title, and it arrives photographed, faded, and stamped, rarely a clean form.

The VIN, engine, and make and model on the title have to match the actual vehicle in the photos, or you are financing a cloned, swapped, or misrepresented unit.

The name on the title, the IDs, the payslip, and the utility bill all have to be the same person, and the proof of residence has to be recent, checks done by eye, document by document.

An already-encumbered title, an out-of-policy vehicle age, or an LTV over your cap all have to be caught the same way on every application and every branch.

THE VEHICLE FILE

Ownership, identity, valuation, and the borrower's capacity: the whole file read into clean, validated data, document by document.

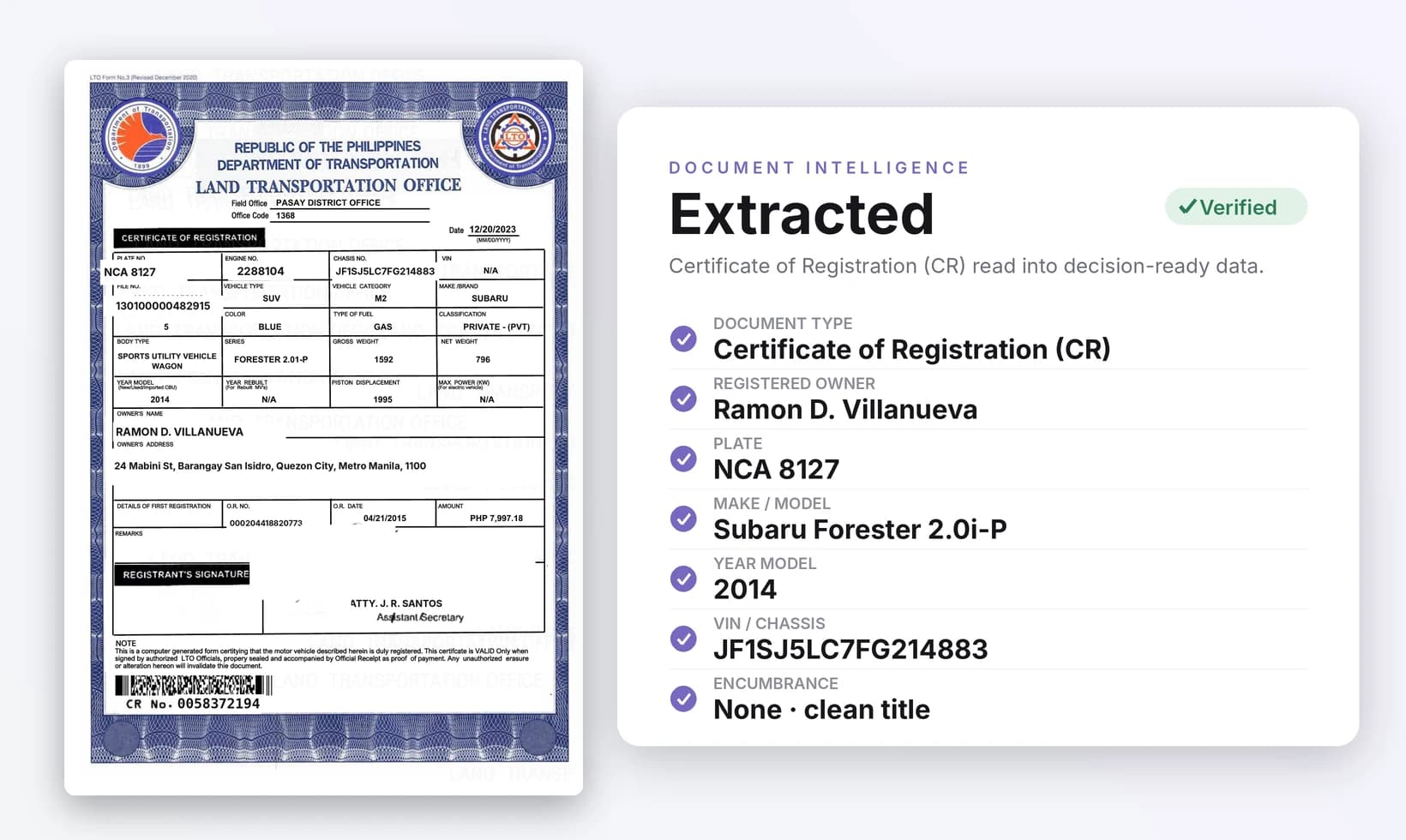

DOCUMENT INTELLIGENCE

Vehicle paperwork rarely arrives clean. Floowed reads the ORCR, title, and deed of sale across the full quality range, where basic OCR and generic IDPs stop at born-digital documents.

Basic OCR / IDP

stops at clean, born-digital

Floowed

reads the whole range

DOCUMENTS TO DECISION

Floowed runs the full path on every application, the same way every time.

DOCUMENTS

Whatever arrives

ORCR or title, deed of sale, vehicle and VIN-plate photos, IDs, payslip, utility bill: photographed, scanned, faded.

CROSS-CHECK

Read and reconciled

VIN, make, and model matched to the vehicle; the name reconciled across every document; the lien and the proof-of-residence date checked.

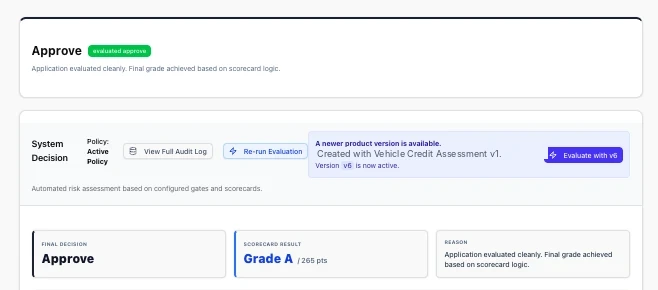

DECISION

Your policy, enforced

Your LTV, vehicle-age, clean-title, and match rules run on every file: approve, refer, or decline, with the reasons on record.

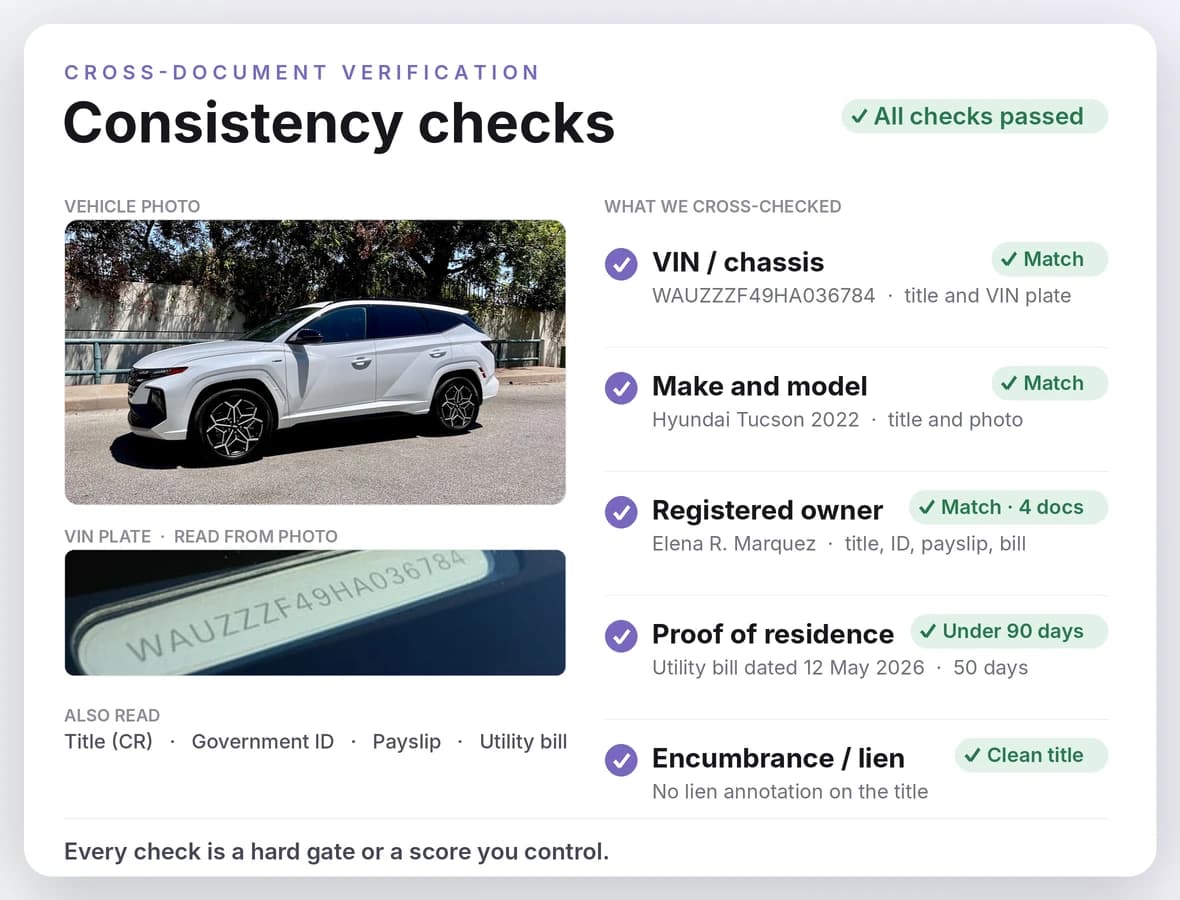

CROSS-DOCUMENT VERIFICATION

A vehicle file only holds up if the documents agree. Floowed reads the ORCR or title, the VIN-plate photo, the vehicle photos, the IDs, the payslip, and the utility bill, then cross-checks them: the VIN and chassis on the title against the VIN plate, the make and model against the actual vehicle, the borrower's name across every document, and the proof of residence against your recency rule. Every check is a hard gate or a score you control, so a cloned unit, a swapped plate, a mismatched name, or a stale utility bill is caught before it reaches a credit officer. The paper, the metal, and the person all have to agree.

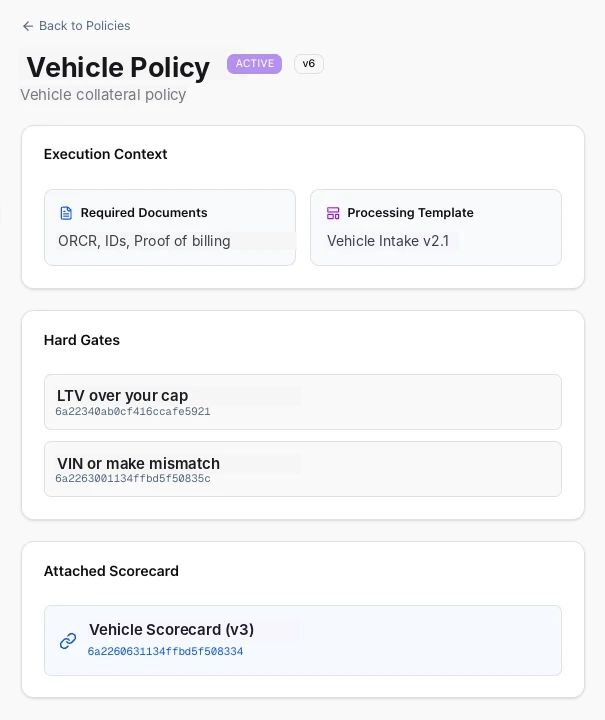

ENFORCEMENT

Encode your vehicle policy once, then let it run. Floowed caps the loan to your LTV against the appraised value, enforces your vehicle-age and year-model cutoffs (and brand-origin rules for heavier units), requires a clean title with no existing lien, and requires the VIN, make, and owner to reconcile before anything is approved. The policy you write is the policy that runs, identically, on every application, on data machine-read from the documents. Every decision carries its reasons, and every policy change is versioned with a full audit trail. Same policy. Every application. Every time. No exceptions.

SPEED

Vehicle lending is won at the point of sale. Floowed turns a title, a set of vehicle photos, and the borrower's documents into a decision in minutes, not the hours a manual file review and a branch appraisal take. Every approval, decline, and referral comes with the full reason record behind it, so nothing is a judgement call no one can reconstruct later.

THE FLOOWED DIFFERENCE

90%

Less time per application

DOCUMENT TO DECISION

99%+

Extraction accuracy, any quality

PHOTOGRAPHED OR FADED

100%

Same policy, every application

FULLY AUDITABLE

WHAT YOU LEND

One decisioning setup across the products vehicle lenders actually run.

Lend against the title while the borrower keeps and uses the vehicle. The ORCR read, matched to the unit, and checked for a clean lien, with refinancing on the same rails.

Underwrite the purchase against an appraised value and your LTV, with the unit verified against its papers before funding.

Heavier units with their own year-model and brand-origin rules, valued and verified the same way, on the same policy.

Decision a book of vehicles at once, each unit read, matched to its title, and run against your policy, not one spreadsheet at a time.

QUESTIONS

Yes. The ORCR (Official Receipt / Certificate of Registration) and equivalent title and registration documents are core vehicle documents Floowed is built to read, including photographed, faded, and stamped pages. It extracts the registered owner, plate, VIN and chassis, engine number, make, model, year, and the encumbrance annotation into validated data.

Yes. Floowed matches the VIN, chassis, and engine number on the title to the photo of the VIN plate or etching, and the make, model, and year to the photos of the vehicle. Mismatches are surfaced as fraud signals, a cloned, swapped, or misrepresented unit, before the application reaches a credit officer.

Yes. Floowed reconciles the name across the title, the government IDs, the payslip, and the utility bill, so a file where the registered owner is not the borrower, or the documents belong to different people, is caught automatically. You decide whether a name mismatch is a hard decline or a score that routes the file for review.

Yes. Floowed reads the date on a utility bill or proof of billing and checks it against your recency rule, for example under 90 days old. A stale document fails the gate or lowers the score, whichever your policy sets, so proof of residence is verified rather than just collected.

Yes. The encumbrance or mortgage annotation on the title shows whether the unit is already financed. Floowed reads it and applies your clean-title rule automatically, so an already-mortgaged vehicle is gated before it can be financed twice.

You set the rules, Floowed runs them. It caps the loan to your loan-to-value against the appraised value, and enforces your vehicle-age and year-model cutoffs (and brand-origin rules for heavier units) on every application, with the unit and the values recorded on the decision.

Yes. OR/CR collateral lending, where the borrower keeps the vehicle and the title is the collateral, is a core use case. Floowed reads the ORCR, matches it to the unit, checks for a clean lien, and runs your policy, including refinancing of an existing unit.

Floowed runs your valuation into the decision. Bring your appraisal, a book or market value source, or your own valuation model, and Floowed feeds it into the LTV calculation and your policy. We orchestrate the decision, we don't replace your valuation.

Yes. A fleet is a book of vehicles, and Floowed decisions each unit the same way: title read, VIN and make matched to the vehicle, name and lien checked, and your policy applied, across the whole book rather than one spreadsheet at a time.

No. Floowed runs your policy. You set the LTV caps, vehicle-age limits, clean-title rules, and matching requirements, and Floowed enforces them on every application, with version history and an audit trail. It is the engine that applies your policy, not a scoring model that overrides it.

Basic OCR reads text off a page and stops there. Floowed reads vehicle documents of any quality, cross-checks the title against the vehicle and the rest of the file, checks the lien, validates the data, then feeds the clean result into your own credit policy to reach a decision, with the documents, the data, and the reasons all on record. It is a loan decisioning platform, not an isolated extraction tool.

ONE PLATFORM

The file is data now. Here's what runs on it.

Upload an ORCR, a photo of the car, and the borrower's documents. Watch Floowed match the VIN, reconcile the file, and reach a decision.